You know that feeling, right? That little financial anxiety when you check your bank account and realize you’ve got almost nothing saved. It’s tough. You want to save, but honestly, where is the money supposed to come from? For a lot of us, we’re living paycheck-to-paycheck. You just can’t find that extra cash. If you’re looking for a structured way to fix that, you need a savings challenge. We’re going to tackle the famous 52-Week Challenge, but we’re going to use your favorite cashback apps to accelerate your savings to over $5,000. Seriously.

Transparency Note: My Cash Back Reviews is an independent site. I personally test money-saving challenges and cashback platforms to provide honest, practical guidance. This post contains affiliate links; if you use my links to sign up for tools I recommend, I may earn a small commission at no additional cost to you, which helps support this site.

📅 The Core Savings Challenges: Picking Your Perfect Pace

The secret to saving money isn’t willpower; it’s consistency. These two challenges give you that structure, and honestly, they work like magic.

1. The 52-Week Savings Challenge (The Classic)

This is the one you see everywhere, and there’s a reason for that. It’s brilliant. You save according to the week number: $1 on Week 1, $2 on Week 2, and so on, until you hit $52 on Week 52.

- The Result? You end up with $1,378! That’s a nice chunk of change for a vacation or maybe an emergency fund.

- A quick tip: I think it’s actually easier to reverse the challenge. You save $52 in January when you’re motivated, and then you’re only putting away $1 or $2 around the holidays when money is tight.

2. The Bi-Weekly Savings Challenge (A Better Fit for Paychecks)

If you get paid every two weeks—which most people do—the Bi-Weekly Challenge is probably a better fit for your budget. You only have to make 26 deposits a year, not 52! You could set a goal to save $100 every two weeks, which is a lot easier to wrap your head around, you know?

- The Result? If you save just $100 every two weeks, you’ll have $2,600 by the end of the year. Way more than the traditional 52-Week Challenge, and it aligns perfectly with your payday schedule.

💸 The Secret Weapon: Let Cashback Apps Fund Your Goal

Here’s where the magic of MyCashBackReviews comes in. Most people quit their saving challenge because they have to use their own money every week. But what if you could fund the deposit with money you earned back on things you bought anyway?

In my experience, this is the only way to accelerate your savings to $5,000 or more.

A. Fund It With Passive Income

You don’t always have to do anything to earn cash back. Seriously. It’s like finding a twenty in an old jacket, but it happens monthly.

- The Strategy: Set up Passive Cashback Apps that work in the background. When that monthly payout hits your bank account, I’m not entirely sure, but I bet it’s enough to cover four weeks of your 52-Week Challenge!

- The Action: Take the money you earn from those “set it and forget it” apps and immediately transfer it into your savings fund. Boom. Challenge funded.

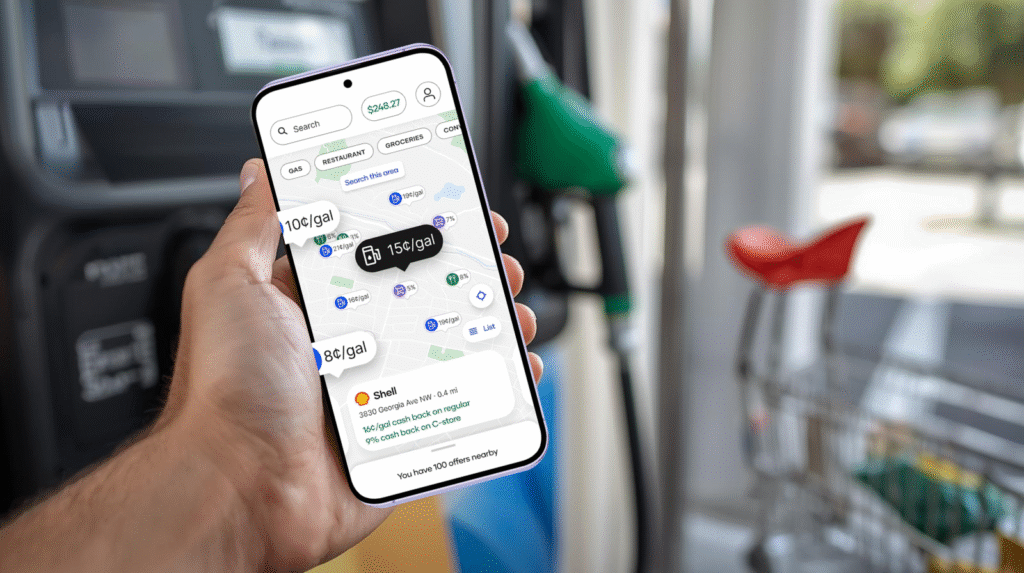

B. Fund It With Gas & Groceries

Gas and groceries are huge budget drains, but they are also massive cashback opportunities.

- The Strategy: Use apps that turn routine expenses into cash deposits. Think about the savings you could earn back on every trip to the pump! The $5 to $15 you get back on gas and groceries is the exact cash you need for your weekly savings deposit.

- The Action: Don’t let that cash disappear. Sign up for Cashback on Gas? Yes (like Upside) and see how much you can earn back on essentials using Fluz = 25% Back.

C. Fund It With Smart Shopping

Look, we all need stuff. But paying full price is, like, a rookie mistake.

- The Strategy: Use coupon codes and cashback deals to create instant savings. That $20 you saved by shopping smart is now $20 you can add directly to your Bi-Weekly Challenge fund.

- The Action: See the savings difference when you compare prices on sites like Temu vs. Amazon. The money you keep is the money you save!

My Personal Take on the 52-Week Challenge

I’ve attempted a few variations of the 52-week challenge, and the biggest lesson I’ve learned is that it’s easy to start in January but difficult to maintain by October. My “Pro-Tip”: Don’t try to save the exact “calendar” amount every week if your income fluctuates. Instead, I use a “cashback-funded” approach. I track my weekly savings goal, but I use the rewards earned from cashback apps to cover the larger, end-of-year deposits. This takes the pressure off your primary paycheck and makes hitting that $5,000 goal feel much more achievable.

🎁 Conclusion: The Cashback Acceleration Method: Fund Your Savings Challenge

You don’t need a crazy finance degree or a six-figure salary to hit a $5,000 savings goal. You just need a solid plan—like the 52-Week or Bi-Weekly Challenge—and a stack of cashback apps working hard to fund your deposits.

I think if you stick to this combination, you won’t just hit your goal, you’ll actually crush it. You’ve totally got this!

Frequently Asked Questions

Q: Is it realistic to save $5,000 in one year? A: It is absolutely possible, but it requires discipline. If you are struggling to hit the weekly targets, the most effective strategy is to “stack” your savings by using cashback apps for your regular shopping. This allows you to supplement your manual savings with “found money” from rewards.

Q: What if I miss a week? A: Don’t quit! The beauty of this challenge is its flexibility. If you miss a week, simply add that amount to your next deposit or spread it out over the remaining weeks. The goal is to build the habit, not to have a perfectly consecutive streak.

Q: How do I keep my challenge money separate? A: I highly recommend opening a dedicated high-yield savings account just for this challenge. Keeping these funds separate from your main checking account reduces the temptation to “borrow” from your challenge savings when life happens.